Istasna najeeb alhuda

Download as PPT, PDF•4 likes•2,253 views

Istisna is a sale transaction where a commodity is agreed upon before its existence and requires specific conditions including using the manufacturer's own materials. Unlike salam, istisna does not require full payment in advance and allows for installment payments, with the option for cancellation before work starts. It also involves risk management through guarantees and allows financing for various applications such as housing and project financing.

Istasna najeeb alhuda

- 1. Istisna Presented by: Muhammad Najeeb Khan (Shriah Advisor) in Habib Metropolatin Bank Islamic Banking

- 2. Introduction Istisna’ is sale transaction where commodity is transacted before it comes into existence. Definition It is an order to producer to manufacture a specific commodity for the purchaser.

- 3. Conditions of Istisna (1)the subject of Istisna is always a thing which needs manufacturing (2)Manufacturer use his own material (3)Quality and Quantity should be agreed in absolute term (4)purchase price should be fixed with mutual consent

- 4. Price of Istisna price of istisna may be in the form of money,commodity and usufruct. Price of Istisna may be spot and differed therefore Istisna is applicable where Salam is not applicable. Price of Istisna is can be paid in installments. The installments may be tied up with different stages of projects. Option When the required goods have been manufactured by the manufacturer purchaser can exercise his option of defect,but he cant use his option of seeing,

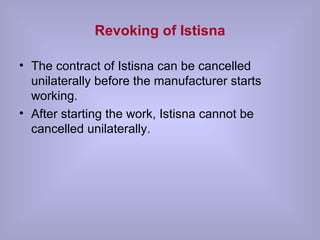

- 5. Revoking of Istisna The contract of Istisna can be cancelled unilaterally before the manufacturer starts working. After starting the work, Istisna cannot be cancelled unilaterally.

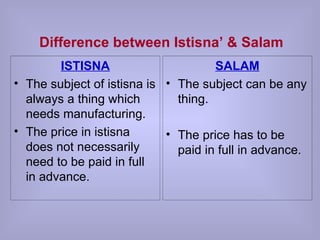

- 6. Difference between Istisna’ & Salam ISTISNA The subject of istisna is always a thing which needs manufacturing. The price in istisna does not necessarily need to be paid in full in advance. SALAM The subject can be any thing. The price has to be paid in full in advance.

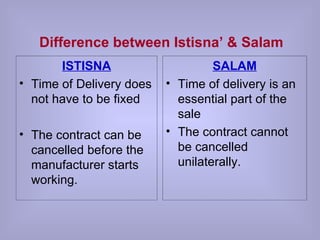

- 7. Difference between Istisna’ & Salam ISTISNA Time of Delivery does not have to be fixed The contract can be cancelled before the manufacturer starts working. SALAM Time of delivery is an essential part of the sale The contract cannot be cancelled unilaterally.

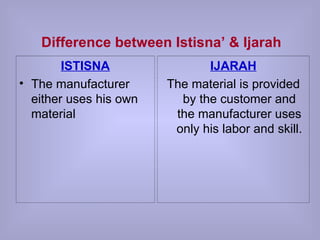

- 8. Difference between Istisna’ & Ijarah ISTISNA The manufacturer either uses his own material IJARAH The material is provided by the customer and the manufacturer uses only his labor and skill.

- 9. Security A security in form of a guarantee, mortgage or hypothecation may be required for Istisna in order to ensure that the manufacturer shall deliver the commodity on the agreed date, in the case of default in delivery,the guarantor may be asked to deliver the same commodity,and if there is a mortgage,the buyer can sell the mortgaged property and the sale proceed can be used either to realize the required commodity by purchasing it from the market,or to recover the price advanced by him.

- 10. Time of Delivery It is not necessary in Istisna that the time of delivery is fixed. However,the purchaser my fix a maximum time for delivery after the appointed time,he will not be bound to accept the goods and pay the price. In order to ensure that the goods will be delivered within the specified period,some modern agreement of this nature contain a penalty clause to the effect that in case the manufacturer delays the delivery after the appointed time,the price shall be reduced by a specified amount per day.

- 11. Delivery of Manufacturing goods Before delivery, goods will remain at the risk of seller. After delivery, risk will be transferred to the purchaser. Possession of goods can be physical or constructive. Transferring of risk and authority of use and utilization/consumption are the basic ingredients of constructive possession. If manufactured goods are delivered before agreed date, purchaser can refuse to accept the goods.

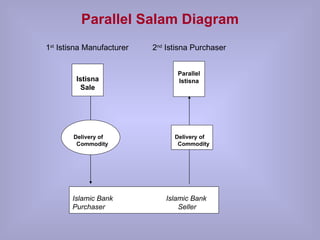

- 12. Parallel Istisna and its applications After the execution of Istisna agreement with one party, buyer or seller executes another Istisna agreement with third party, Conditions for Parallel Istisna : (a) there must be two different and independent contracts, these two contracts cannot be tied up and performance of one should not be contingent on the other. (b) Parallel Istisna is allowed with third party only.

- 13. Parallel Salam Diagram Delivery of Commodity Istisna Sale Parallel Istisna Islamic Bank Islamic Bank Purchaser Seller 1 st Istisna Manufacturer 2 nd Istisna Purchaser Delivery of Commodity

- 14. Potential of Istisna The client can get finance for raw material, working capital and other overhead expenses by the execution of Istisna agreement. House financing, import and export products can be easily designed on Istisna basis.

- 15. Istisna as Mode of Financing House Financing Project Financing BOT Arrangement Export Pre Shipment

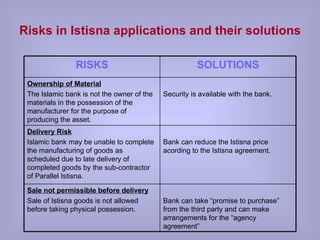

- 16. Risks in Istisna applications and their solutions RISKS SOLUTIONS Ownership of Material The Islamic bank is not the owner of the materials in the possession of the manufacturer for the purpose of producing the asset. Security is available with the bank. Delivery Risk Islamic bank may be unable to complete the manufacturing of goods as scheduled due to late delivery of completed goods by the sub-contractor of Parallel Istisna. Bank can reduce the Istisna price acording to the Istisna agreement. Sale not permissible before delivery Sale of Istisna goods is not allowed before taking physical possession. Bank can take “promise to purchase” from the third party and can make arrangements for the “agency agreement”